Introduction

The introduction of corporate tax law in the UAE marks a significant shift in the financial landscape of the region.

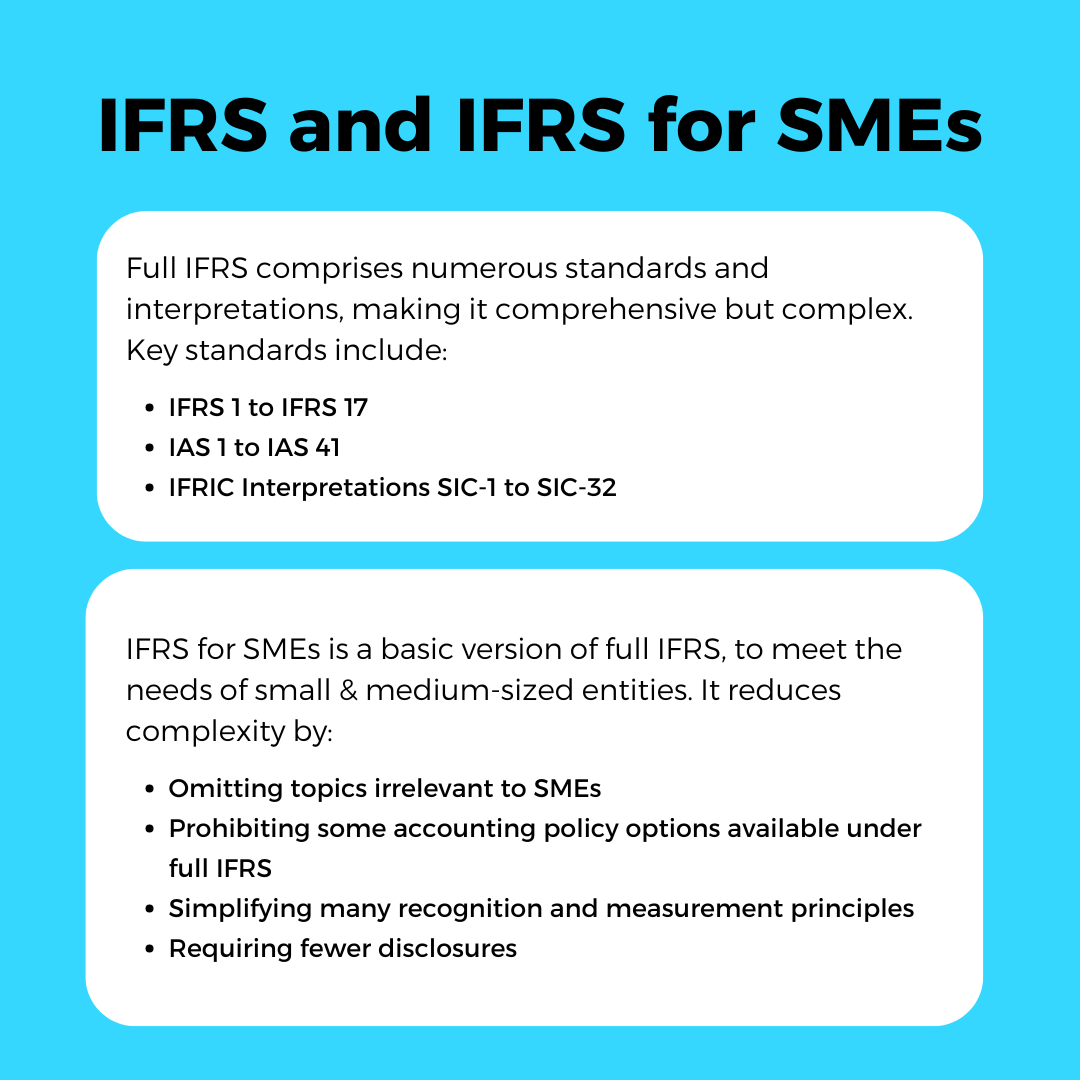

Central to this shift is the adherence to International Financial Reporting Standards (IFRS) and their variant for small and medium-sized entities (IFRS for SMEs).

This article aims to provide an in-depth analysis of the requirements under the new corporate tax law, as stipulated in the Ministerial Decision No. 114 of 2023, and how these align with IFRS principles.

Overview of IFRS

International Financial Reporting Standards (IFRS) are globally recognized accounting standards developed by the International Accounting Standards Board (IASB).

They provide a uniform framework for financial reporting, enhancing comparability and transparency across different jurisdictions.

IFRS is widely adopted, with approximately 120 nations either permitting or requiring IFRS for domestic listed companies.

UAE Corporate Tax Law

The UAE’s new corporate tax law, detailed in Federal Decree-Law No. 47 of 2022, mandates specific accounting standards for different categories of taxable entities.

The Ministerial Decision No. 114 of 2023 outlines these requirements, emphasizing the use of IFRS and IFRS for SMEs based on the entity’s revenue.

- Turnover of AED 50 million and above: Entities in this category must adopt full IFRS.

- Turnover above AED 3 million but less than AED 50 million: These entities are required to use IFRS for SMEs.

- Turnover below AED 3 million: No IFRS standards are mandated; these entities may prepare their financial statements on a cash basis.

Notably, IFRS for SMEs excludes standards such as IFRS 9 (Financial Instruments), IFRS 15 (Revenue from Contracts with Customers), and IFRS 16 (Leases).

Key Provisions of Ministerial Decision No. 114 of 2023

The Ministerial Decision No. 114 of 2023 lays down crucial guidelines for the application of accounting standards under the UAE’s Corporate Tax Law. This decision is essential for ensuring that taxable entities comply with standardized financial reporting practices, thus facilitating accurate and transparent tax calculations. Key provisions include:

- Financial Statements: Entities must prepare a complete set of financial statements as per the applicable IFRS or IFRS for SMEs. This includes statements of income, other comprehensive income, balance sheets, changes in equity, and cash flow statements.

- Cash Basis Accounting: Entities with revenue below AED 3 million can prepare financial statements using the cash basis of accounting, recognizing income and expenditure when cash is received or paid.

- Consolidated Financial Statements: For tax groups, consolidated financial statements must be prepared by aggregating the standalone financial statements of the parent company and each subsidiary, eliminating intra-group transactions.

- Applicable Standards:

- Full IFRS is mandatory for entities with revenue exceeding AED 50 million.

- IFRS for SMEs can be applied by entities with revenue up to AED 50 million.

Implications for Taxable Income Calculation

Adjustments are required when calculating taxable income to align with the corporate tax law. For instance, entities must replace the equity method of accounting with the cost method where applicable.

Under IFRS, the equity method is used when an investor has significant influence over an investee, recognizing its share of profits or losses.

The cost method, conversely, is used when there is no significant influence, recording investments initially at cost and adjusting for value changes like impairments.

Conclusion

The implementation of corporate tax law in the UAE, along with the mandated adoption of IFRS, represents a crucial development for businesses operating in the region.

Understanding these requirements and ensuring compliance will be essential for accurate financial reporting and tax calculation.

As the UAE continues to refine its corporate tax framework, businesses must stay informed and adapt to any new guidelines or amendments issued by the authorities.

We advise you to consult with a Tax Advisor like Growbox.